Home insurance covers roof damage when it's caused by a sudden, accidental event your policy lists as a covered peril — not when it's the slow result of age or poor maintenance. This single distinction is the foundation of every roof claim I've ever worked, and it's where most confusion starts.

What roof damage is typically covered

Standard homeowners policies in Ohio generally cover roof damage from "covered perils" — the sudden events insurers agree to pay for. Around Reynoldsburg and the greater Columbus area, the ones we see most are:

- Wind damage — shingles lifted, creased, or torn off during a storm

- Hail damage — bruised, cracked, or fractured shingles (our late-spring hail season is the single biggest driver of local claims)

- Falling trees or debris — a limb through the deck after a windstorm

- Fire and lightning — direct damage to roofing materials

If a covered peril damages your roof, your policy is designed to help pay for the repair or replacement, minus your deductible.

What roof damage is usually NOT covered

Insurance won't pay to replace a roof that simply wore out. General wear and tear, age-related deterioration, granule loss, curling shingles, and damage from deferred maintenance are considered the homeowner's responsibility — not an insurable loss. This is exactly why a roof's age matters so much: the older the roof, the easier it is for an adjuster to attribute damage to age rather than weather.

"Age doesn't disqualify a claim — the cause of the damage does. A 22-year-old roof that got hammered by a May hailstorm has a real claim. The mistake I see is homeowners waiting months to report it, until the damage starts looking like wear instead of weather." — Ethen Steele, Owner & HAAG Certified Inspector

Will Insurance Cover a 20-Year-Old Roof?

Insurance will cover a 20-year-old roof if your policy was already active, you accurately disclosed the roof's age, and the damage came from a covered peril. What changes at 20 years isn't your eligibility — it's how generously you'll be paid and how closely your insurer watches your roof at renewal.

How roof age changes your coverage

A 20-year-old asphalt roof sits right at the edge of what most carriers consider insurable. As a roof passes the 15-to-20-year line, insurers commonly do one of three things: require a roof inspection before renewing, switch the roof from replacement cost to actual cash value, or decline to write a brand-new policy on it at all. None of that means an existing, in-force claim gets denied automatically — but it does mean your roof is now flagged as higher risk, which can show up as higher premiums or a non-renewal notice.

ACV vs. RCV: the difference that costs homeowners thousands

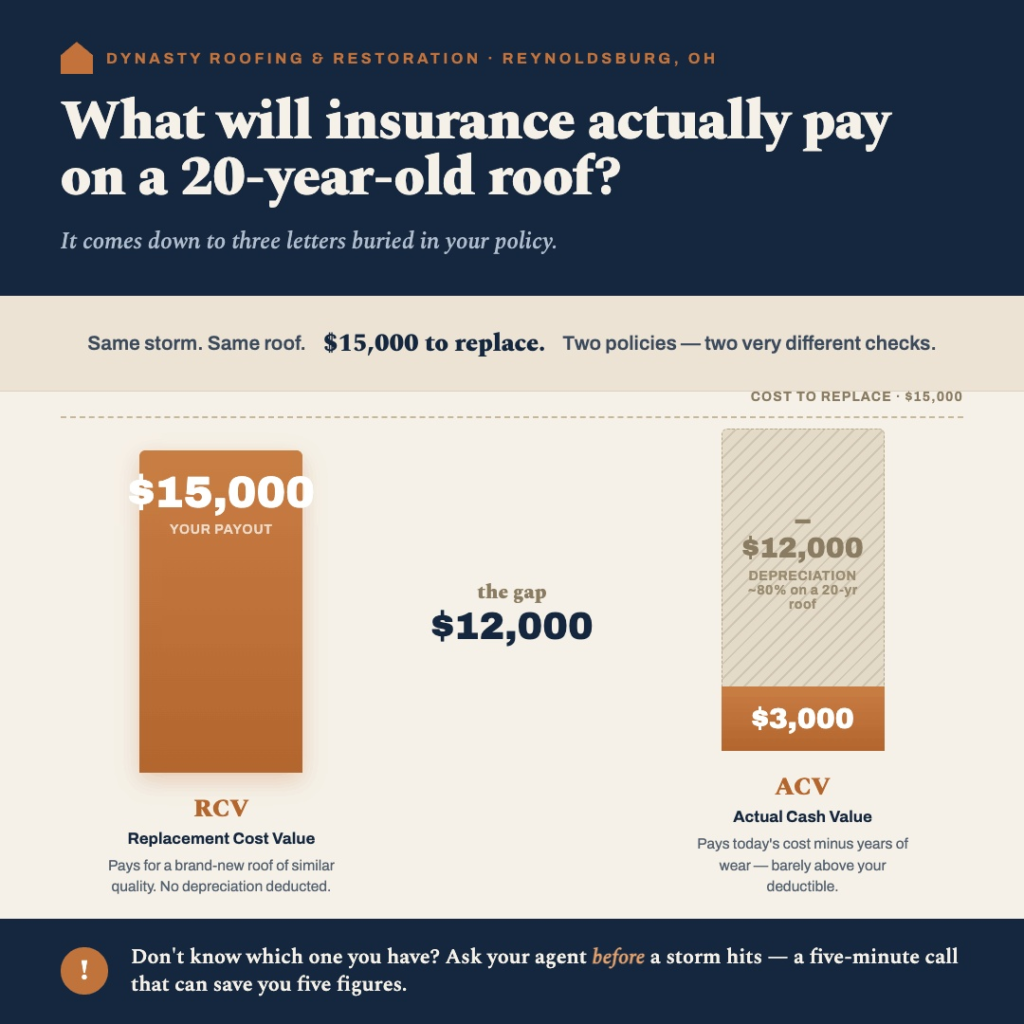

The most important line in your policy is whether your roof is insured at Replacement Cost Value (RCV) or Actual Cash Value (ACV) — because on an older roof, they produce wildly different checks.

- RCV pays to replace your roof with a new one of similar quality, minus your deductible. Depreciation isn't deducted (though it's often held back and released after the work is done — more on that below).

- ACV pays the depreciated value of your roof — today's replacement cost minus years of wear. On a 20-year-old roof, depreciation can erase the majority of the payout.

Here's a real-world example I walk homeowners through:

I've stood in plenty of Reynoldsburg living rooms and watched a homeowner's face drop when they learn their 'covered' roof only pays out a few thousand dollars. The policy didn't lie to them — they just never knew the difference between actual cash value and replacement cost until the check showed up." — Ethen Steele

If you're not sure which one you have, call your agent and ask before you ever need to file. It's a five-minute conversation that can save you five figures. For more on how we document storm damage to support these claims, see our Reynoldsburg storm damage roof repair page.

Does Homeowners Insurance Cover Roof Leaks?

Homeowners insurance covers a roof leak when the leak results from a covered peril — but not when it results from age, wear, or a maintenance problem you let slide. So a leak the morning after a hailstorm is a very different claim than a leak that's been slowly staining your ceiling for two years.

When a roof leak IS covered

If a windstorm tears off shingles and rain pours through the opening, or hail cracks the surface and water finds its way in, that leak traces back to a covered peril — and the resulting interior water damage is often covered too. The key is a clear, sudden cause and prompt reporting.

When a roof leak is NOT covered

A leak caused by old, brittle shingles, failed flashing nobody maintained, or an ice dam during one of our Ohio freeze-thaw cycles is typically treated as wear and tear or a maintenance issue. Insurers will often deny these, arguing the homeowner had time to catch and fix the problem. That's why our annual inspections check flashing, seals, gutters, and shingles — catching the small stuff before it becomes an uncovered claim.

Does Insurance Cover Roof Replacement, or Just Repairs?

Insurance covers a full roof replacement when covered-peril damage is widespread enough that repairs won't restore the roof, and it covers roof repairs when the damage is localized. The adjuster's job is to determine which scenario applies — and that determination isn't always final.

When insurance pays for a full replacement

If a storm damages a large portion of your roof, or the damage compromises the roof's integrity, a full replacement may be approved. Isolated damage — a few missing shingles, one small leak — usually gets repaired instead. Two things can tip a borderline claim toward full replacement: documentation showing the damage is more extensive than the first inspection found, and Ohio's roof matching rule.

Ohio's roof matching law (Admin. Code 3901-1-54)

Ohio's roof matching provision can require your insurer to pay for a uniform result, not a patchwork one. Under Ohio Administrative Code 3901-1-54, insurers are expected to repair damaged areas with materials of "reasonably comparable appearance" to the rest of your roof. If your shingles are discontinued or so weathered that new ones can't reasonably match, that rule can push a partial claim toward a full replacement. It's not automatic — courts have sided with insurers when homeowners couldn't show the repair would look mismatched — so documentation matters here too. This is one of the most underused tools Central Ohio homeowners have, and it's worth raising with your adjuster.

When a replacement is genuinely the right call, we install IKO Performance asphalt shingles built for Ohio's weather, backed by IKO's Iron Clad® Protection Period. You can learn more about our process on our Reynoldsburg roofing page.

What Should I Do If My Insurance Denies My Roof Claim?

If your insurance denies your roof claim, don't treat the denial as final — review the denial letter, gather stronger evidence, and file a formal appeal. In my experience, a well-documented appeal succeeds far more often than homeowners expect, because the original denial is frequently based on an incomplete inspection.

Step-by-step: appealing a denied roof claim

- Get the denial in writing. Request a formal denial letter stating the specific reason and the exact policy language cited. This is your roadmap.

- Re-read your policy. Confirm whether your damage falls under a covered peril, and check for a cosmetic-damage exclusion or a percentage deductible that may explain the decision.

- Get independent documentation. A second, professional inspection — ideally from a HAAG Certified inspector — produces the photos, measurements, and report that counter an incomplete adjuster assessment.

- File a written appeal. Reference your claim number and the denial date, state your disagreement plainly, and attach your new evidence. Move fast — appeal windows can be as short as 30 to 60 days.

- Escalate if needed. You can file a complaint with the Ohio Department of Insurance, which oversees how carriers handle claims, or consult a public adjuster or attorney for suspected bad-faith denials.

Your rights and deadlines in Ohio

Ohio sets minimum standards your insurer can't dip below. Under the state's claim-handling rules, insurers are generally expected to acknowledge a claim within 15 days and make a coverage decision within 21 days of receiving your proof of loss. And if a dispute ends up in court, Ohio gives you six years from the date of loss to file a breach-of-contract action (reduced from eight years in 2021). Knowing these timelines keeps an insurer from quietly running out the clock on you.

"A denial letter isn't a verdict — it's an opening position. Half the denials I've helped overturn came down to one thing: the adjuster's report was incomplete, and nobody pushed back with better documentation." — Ethen Steele

When you're documenting a storm claim, having a local roofer who works with every major carrier in your corner makes a real difference. That's a core part of how we help Reynoldsburg homeowners with insurance claims.

Frequently Asked Questions

Will insurance cover a roof that's more than 20 years old?

It can, but it gets harder. Many insurers won't write a new policy on a roof past 20 years, and those that do often cover it at actual cash value only. If your existing policy is already in force and you disclosed the roof's age, covered-peril damage should still be covered.

Does home insurance cover roof leaks from old age?

No. Leaks caused by aging shingles, worn flashing, or general deterioration are considered maintenance issues and are typically excluded. Leaks caused by a covered peril — like wind or hail — are usually covered, including the resulting interior water damage.

How do I prove my roof damage was caused by a storm and not age?

Document it fast and thoroughly. Date-stamped photos, a professional HAAG Certified inspection, and prompt reporting after the storm all help establish a sudden cause. The longer you wait, the easier it is for an adjuster to attribute the damage to wear.

Will filing a roof claim raise my insurance rates?

It can, and an older roof already carries higher risk in an insurer's eyes. That said, the protection a legitimate claim provides usually outweighs the rate impact. Ask your agent how a claim would affect your specific policy before deciding.

Should I replace my older roof before I lose coverage?

If your roof is near the end of its lifespan, a proactive replacement can restore full replacement-cost eligibility, lower your premium, and prevent a non-renewal. We'll tell you honestly whether replacement, repair, or rejuvenation makes the most sense after an inspection — we don't sell roofs people don't need.

The Bottom Line on Older Roof Coverage

So, will insurance cover a 20-year-old roof? In most cases, yes — as long as your policy is active, you were honest about the roof's age, and the damage came from a covered peril rather than ordinary wear and tear. The real story is in the fine print: whether you're insured at replacement cost or actual cash value can mean the difference between a new roof and a check that barely covers your deductible. Knowing where you stand before a storm hits is the single best thing you can do to protect your home and your wallet.

And if your claim gets denied? That's not the end of the road. With the right documentation, a second inspection, and Ohio's homeowner protections on your side, plenty of "no" answers turn into "yes."

Get an Honest Look at Your Roof — and Your Coverage

If your roof is aging or you've taken recent storm damage, don't guess about your coverage. Dynasty Roofing offers free, no-pressure assessments across Reynoldsburg, Columbus, Gahanna, Pickerington, New Albany, and the surrounding area. As a family-owned, BBB A+ accredited, HAAG Certified team, we'll walk your roof, document exactly what we find, and help you navigate your insurance claim from first call to final payment.

Call (614) 567-3003 or schedule your free assessment today — we'll have someone out by next day.